TOP GLOVE’S NET PROFIT TO REMAIN STRONG IN QFY, SAY ANALYSTS

09 March 2021 / 12:03

KUALA LUMPUR (March 9): Top Glove Corp Bhd’s earnings for the December to February quarter is expected to remain strong. The earnings anticipation is fuelled by stable average selling prices (ASPs) on the back of strong global demand for rubber gloves amidst the Covid-19 pandemic.

KUALA LUMPUR (March 9): Top Glove Corp Bhd’s earnings for the December to February quarter is expected to remain strong. The earnings anticipation is fuelled by stable average selling prices (ASPs) on the back of strong global demand for rubber gloves amidst the Covid-19 pandemic.

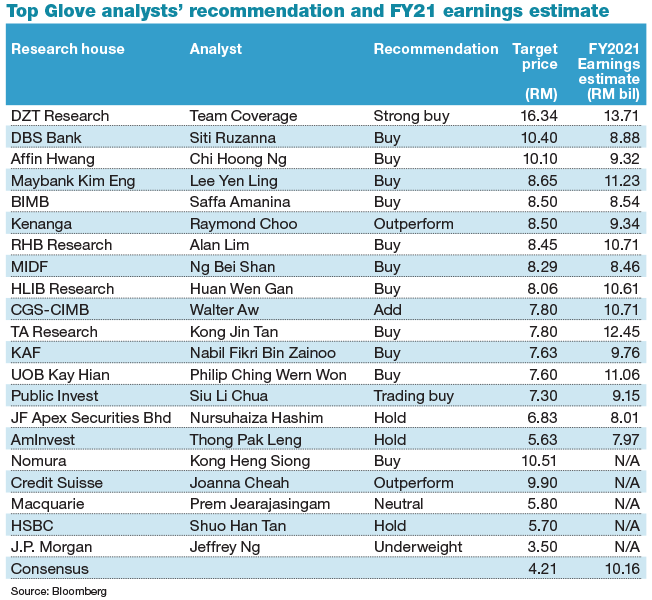

Top Glove will be releasing its result for the second quarter ended Feb 28, 2021 (2QFY21) today. The market consensus forecast Top Glove's annual profit to come in at RM10.16 billion for the financial year ending Aug 31, 2021 (FY21).

Based on Top Glove’s reported net profit of RM2.38 billion in its first quarter ended Nov 30, 2020 (1QFY21), this means it will need to deliver an average of RM2.59 billion for the next three financial quarters, in order to meet analysts’ expectations.

For illustration purposes, if the 2QFY21 net profit comes in at RM2.59 billion, this represents an 8.8% quarter-on-quarter (q-o-q) increase from its 1QFY21 net profit of RM2.38 billion. The growth, however, will be slower compared to 1QFY21, when the company’s net profit grew 84% q-o-q from RM1.29 billion in 4QFY20.

On a year-on-year basis, it would have registered an earnings growth 22 times of the net profit of RM115.68 million in 2QFY20.

Similarly, the market is expecting Top Glove to post record annual revenue with the consensus estimate of RM21.35 billion. The company is expected to achieve a quarterly revenue of RM5.53 billion for the upcoming three quarters, after it posted a revenue of RM4.76 billion in 1QFY21. Top Glove reported a revenue of RM1.23 billion in 2QFY20.

When contacted, Rakuten Trade Research head of equity sales Vincent Lau said his expectation for Top Glove’s upcoming quarterly earnings is in line with market consensus of a robust set of financials in 2QFY21.

As the market has priced the catalyst for its strong quarterly earnings for 2QFY21, hence there will be no positive earnings surprise, he noted.

“I think investors want to know whether or not the company’s glove average selling price (ASP) has peaked and also overcapacity concerns [given the vaccine development], which are the main factors hanging over the glove sectors now,” Lau said.

Meanwhile, a local head of research said a record-breaking quarter can be expected for 2QFY21, with a projected net profit topping RM3 billion.

“Top Glove is likely to achieve record earnings, but the growth will be capped below 30% (q-o-q),” he said.

He attributed the earnings growth to rising ASP for gloves – albeit only marginally better than the previous quarter – on the back of strong demand for gloves globally.

According to him, ASPs for glove products has still not yet reached its peak, given that the vaccination programme has only started in some countries back in December 2020.

MIDF Research analyst Ng Bei Shan concurred that Top Glove’s ASP glove products “will be holding up until the first half of calendar year 2021 (1HCY21)”, depending on how the pandemic develops over time.

“We had previously anticipated that ASPs may soften in 2HCY21 and that the adjustment in ASPs is likely to be gradual. That is because based on our projection, demand for gloves is likely to continue to exceed supply for 2021 and likely into 2022. As such, we do not expect ASPs to revert to pre-pandemic level so soon,” she told The Edge.

“(Hence) We still have a BUY recommendation on Top Glove, with a target price of RM8.29,” she noted.

Ng has forecasted Top Glove to deliver an annual net profit of RM8.46 billion for FY21, which means the company will need to deliver a net profit of RM2.12 billion per quarter, in order to meet her expectation.

“Downside risks include spike in raw material prices, surprise disruption to supply chain or operations, sooner than expected ending of the pandemic and lukewarm response to its Hong Kong dual listing,” she said.

To put things into perspective, both Hartalega Holdings Bhd and Supermax Corp Bhd saw strong growth in their latest quarterly results, driven by higher ASPs and robust demand.

Hartalega saw its net profit for the third quarter ended Dec 31, 2020 (3QFY21) leap to a record high of RM1 billion, up nearly 84% against RM544.96 million in the preceding quarter, 2QFY21. Its revenue grew by 58.2% to RM2.13 billion quarter-on-quarter (q-o-q) against RM1.35 billion in 2QFY21.

Supermax Corp Bhd reported a record net profit of RM1.06 billion for the second quarter ended Dec 31, 2020 (2QFY21), a 34% quarter-on-quarter jump from RM789.52 million in 1QFY21. Quarterly revenue surged to RM2 billion, compared with RM1.35 billion in the preceding quarter.

Meanwhile, Top Glove’s filing dated Jan 4 stated that the company’s shareholders will receive 70% of the company’s profit after tax and minority interest (PATAMI) as dividend for the second, third and fourth quarters of the FY21 – after it committed to pay special dividend of 20%, on top of the 50% dividend payout ratio on its PATAMI.

A local head of research said the dividend payout ratio of 70% can be expected, given its strong cash position with good earnings in coming quarters.

According to his base case scenario, the company will make a quarterly net profit of RM3 billion or earnings per share of 36.57 sen per share for 2QFY21, while Top Glove shareholders will receive dividend per share of 25.6 sen at a payout ratio of 70%.

For FY21 as a whole, based on back of envelope calculations, Top Glove shareholders will receive dividend per share of 65.98 sen per share at a payout ratio of 70%, based on the earnings consensus of RM10.16 billion or RM1.239 per share for FY21 and after deducting a quarterly net profit of RM2.38 billion or 29.64 sen per share for 1QFY21.

As at Nov 30, Top Glove’s net cash position stood at RM3.45 billion.

Questions for Top Glove

But aside from its financials, investors will be keen to hear the company explain as to why it is planning for a second primary listing in Hong Kong, when it has a growing cash pile.

Also of interest is how it will be affected when glove sales normalise, given it is cut out of the US market with the Customs & Border Protection ban against Top Glove’s products.

Lastly, what is the status of the group’s ESG compliance, especially the condition of workers’ accommodation.

.jpg)

.png)

.png)

.png)

.png)

.png)